You can graduate with a first-class degree and have no idea what is happening inside your own bank account. Millions already have. This is the financial literacy gap in higher education in its starkest form: institutions spend years certifying that a graduate can analyse a legal case, model a chemical reaction, or interpret a novel, while leaving entirely untouched the question of how that same graduate will manage a payslip, a loan, or a pension. When did anyone actually sit you down and explain what compound interest does to a credit card balance left unpaid for a year? For most graduates, the honest answer is never.

This is not a niche concern for economics departments to quietly resolve. It is a lived experience that most readers, or their children, will recognise immediately: the confusion of a first payslip, the anxiety of a student loan statement that nobody fully explained, the slow realisation that a degree certificate says nothing about whether its holder can build a budget that survives contact with real life. The gap is not a failure of intelligence. It is a failure of curriculum design, and it deserves to be treated as seriously as any other subject a university claims to teach.

What Financial Literacy Actually Means: Naming the Financial Literacy Gap in Higher Education

Financial literacy, stripped of jargon, is the practical ability to understand and act on money decisions that affect daily life and long-term security. It is not a specialised skill reserved for finance graduates. Most of what falls inside this gap requires no advanced mathematics at all, simply structured exposure that the average curriculum never provides.

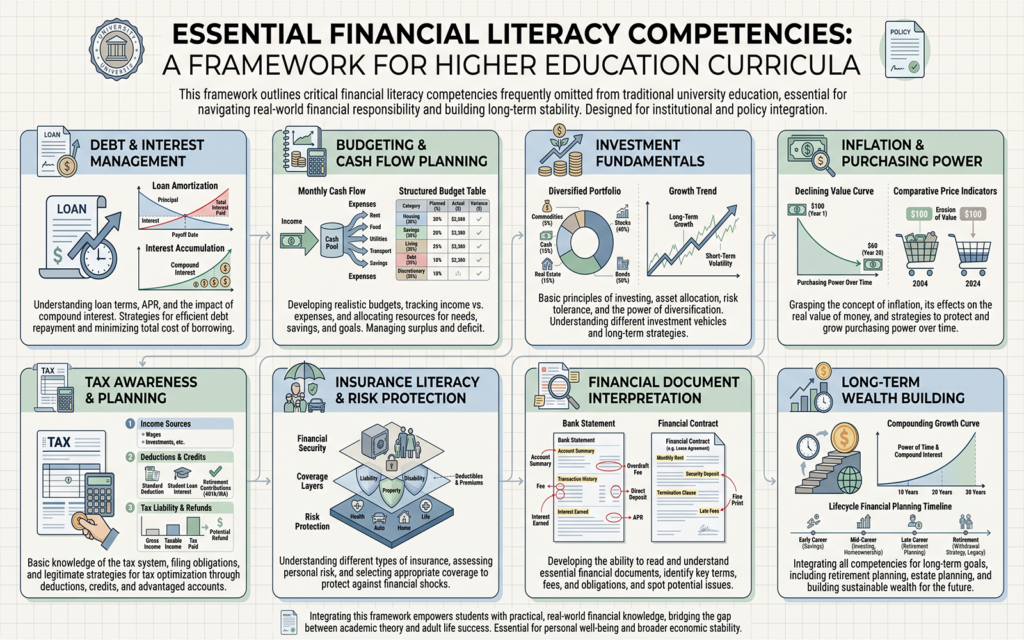

The competencies most graduates lack tend to cluster around five areas:

- Understanding debt, including how interest compounds over time, what a debt-to-income ratio actually means, and how to weigh up a borrowing decision before signing for it.

- Basic investment concepts, such as the difference between savings vehicles, how compound growth works in an investor’s favour rather than against them, and the relationship between inflation, risk, and return.

- Reading financial documents, from a payslip and a tenancy agreement to an insurance policy and a basic balance sheet.

- Budgeting and cash flow, meaning the discipline of managing income against obligations across weeks and months rather than reacting to whatever is left at the end of each one.

- Tax basics, including how income tax actually works, what self-employment changes about a person’s filing obligations, and what a payslip deduction actually pays for.

None of these demands a mathematics degree. It demands a curriculum that decides this was worth teaching in the first place.

The Evidence Behind the Financial Literacy Gap in Higher Education

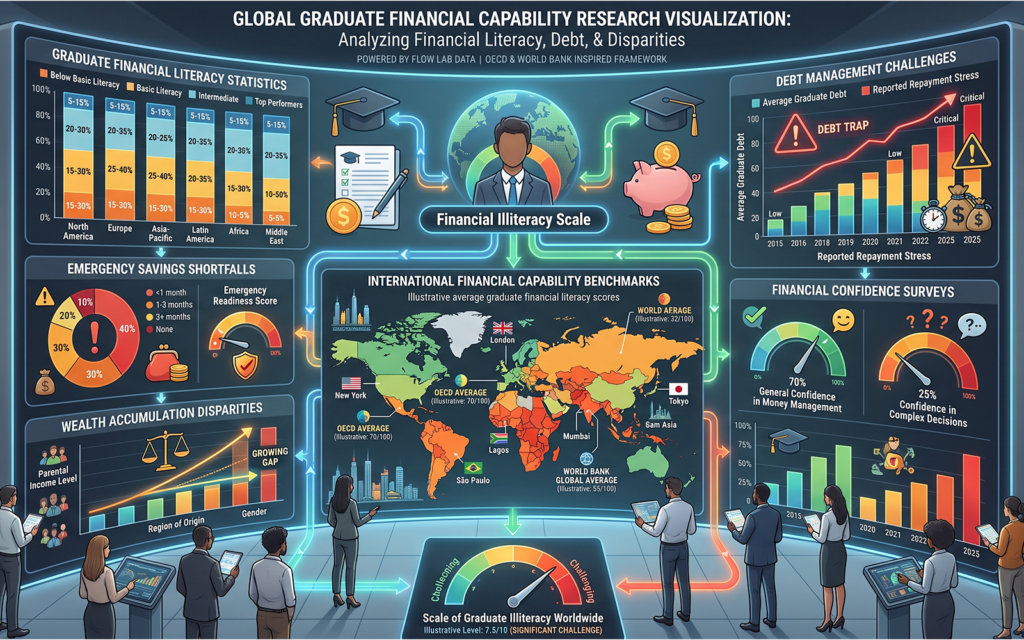

The scale of the problem is well documented, and the documentation is consistent across regions. The OECD’s 2023 International Survey of Adult Financial Literacy found that while seventy-seven per cent of adults across participating countries understood the basic relationship between risk and reward, only forty-two per cent could correctly answer a question about compound interest, arguably the single concept with the greatest long-term effect on both debt and savings outcomes. The UNESCO Institute for Lifelong Learning paints an even starker global picture, noting that only one in three adults worldwide is considered financially literate, with rates falling further in developing regions.

The consequences show up early in adult life. Research summarised in Inside Higher Ed found that only a quarter of students could correctly answer three basic financial literacy questions, with students from lower-income families and those under twenty-one less likely to answer correctly still. On the resilience side, Bank of America’s most recent Better Money Habits study found that fifty-five per cent of Gen Z respondents did not have enough savings to cover three months of expenses, a precarious position for anyone facing an unexpected bill or a gap between jobs. At a global level, the World Bank has found that half of all adults in emerging market and developing economies cannot financially cope with an emergency at all. None of these are extreme outliers. They describe the typical graduate, not the unlucky exception.

Why Universities Have Been Slow to Close This Gap

The reasons institutions have left this gap unaddressed are understandable, even if they are no longer defensible. Curriculum rigidity is the most practical obstacle: adding compulsory content almost always means removing something else, and few departments volunteer to lose teaching hours. Personal finance has also long carried a perceived non-academic status, treated as practical skills training rather than content worthy of credit, even though it requires the same structured reasoning as any applied subject. Many institutions have simply assumed the responsibility belongs elsewhere, with families, schools, or banks expected to fill the gap before a student ever enrols. And finance departments themselves are often staffed to teach corporate finance and economic theory, not the personal financial management that a general undergraduate population actually needs.

This combination of reasons explains why the financial literacy gap in higher education has persisted for decades, largely unchallenged. What has changed is the cost of continuing to ignore it. Graduate debt levels have risen substantially in most major economies, financial products have grown more complex, and the consequences of financial confusion now follow graduates considerably further into adult life than they once did.

The Downstream Consequences for Graduates, Families, and Economies

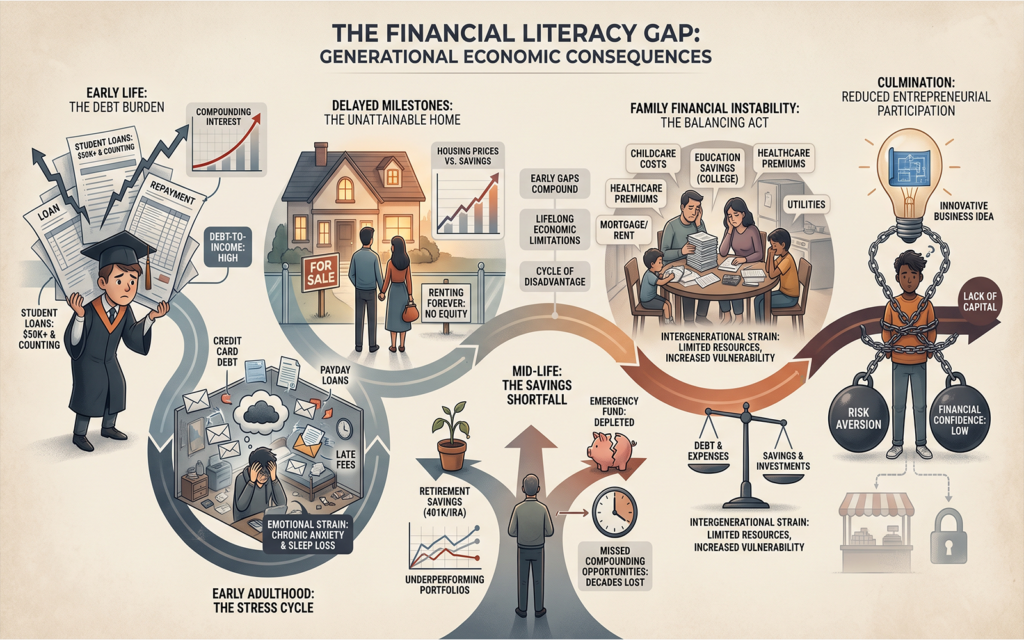

The cost of this gap does not stay contained to a single bad decision. For graduates, small early missteps, an unnecessarily expensive loan, a missed opportunity to save while young, compound into materially lower lifetime wealth in much the same way that unpaid interest compounds against a struggling borrower. For families, financial stress remains one of the most consistently documented drivers of relationship strain, declining mental health, and the kind of intergenerational poverty that a degree was supposed to interrupt. Employers feel it too: financially stressed staff are reliably linked to lower productivity and higher staff turnover, since money worries do not stay confined to evenings and weekends. At an economic level, the World Economic Forum has highlighted financial literacy as a significant global problem precisely because financially capable populations save, invest, and start businesses more readily, the very activity economies depend on for growth. The financial literacy gap in higher education is, in this sense, not a private inconvenience. It is a cost that societies absorb long after the graduation photographs are taken.

Read More: Top Marketing Strategies for Higher Education Institutions to Boost Student Enrolment

The Universities Doing This Well: What a Financial Literacy Curriculum Actually Looks Like

A small number of institutions have already shown that closing this gap does not require a curriculum overhaul, only intent and modest investment. The University of South Florida has required incoming freshmen to complete a financial literacy module since 2009, a response to rising undergraduate debt and loan default rates, and tens of thousands of students have now completed it. Florida State University runs its Unconquered by Debt programme through its Stavros Centre for Economic Education, building financial literacy directly into the student experience rather than treating it as an optional extra. Western Washington University takes a more experiential route, offering a digital badging system across budgeting, credit, savings, and investment that students build up progressively rather than completing in a single sitting.

The common thread across these examples is structure rather than scale: a mandatory first-year module, integration into discipline-specific contexts such as entrepreneurship modules for business students or contract literacy for law students, and tools that make the learning experiential rather than theoretical. None of this requires rebuilding a degree programme from scratch.

Why This Is a Partnership Opportunity, Not Just a Policy Debate

For institutional leaders, this is no longer purely a curriculum debate; it is a competitive one. Universities that build financial literacy into the student experience tend to see stronger graduate employment outcomes and satisfaction data, more engaged alumni networks, and a clearer point of differentiation in increasingly crowded student markets. As graduate employability becomes a more visible institutional metric, in rankings, accreditation reviews, and prospective student decisions alike, financial capability is one of the most tangible, easily communicated proof points an institution can offer.

How EduTech Global Partners With Institutions to Build More Complete Graduates

EduTech Global works with institutions that want to expand their curriculum with high-value practical modules without disrupting existing academic structures, integrating employability and life-readiness content alongside core teaching. That includes helping institutions improve the graduate outcomes data increasingly scrutinised by rankings and accreditation bodies, and positioning themselves as institutions producing graduates ready for the realities of working life, not only its academic requirements. The belief underpinning this work is straightforward: education should produce more than qualified graduates. It should produce capable people.

Closing the Gap Is a Choice, Not an Inevitability

Closing the financial literacy gap in higher education does not require an institution to reinvent its degree structures or sacrifice academic rigour. It requires the same deliberate intent that built every other part of the curriculum: deciding that this subject matters enough to teach properly. For policy makers, curriculum designers, and university leaders, the evidence is no longer ambiguous, and neither is the cost of inaction. EduTech Global partners with institutions ready to build that capability into their graduates from day one. Explore how that partnership works, and contact our team to discuss what it could look like for your institution.

Frequently Asked Questions

Why is financial literacy not taught at university? Most institutions have left it out for structural reasons rather than principled ones: compulsory curriculum space is hard to free up, personal finance has historically been seen as a practical skill rather than academic content, and many universities assumed families, schools, or banks would cover it instead.

What is the financial literacy gap and why does it matter? It is the difference between the financial knowledge a typical graduate needs to manage debt, savings, tax, and contracts, and what their education actually provides. It matters because the gap compounds over decades into lower lifetime wealth, greater financial stress, and weaker economic participation.

Should personal finance be a compulsory university subject? There is a strong practical case for it: the core competencies require no advanced mathematics, can be integrated into existing modules, and institutions that have made it compulsory report measurable improvements in student financial confidence and retention.

How does financial illiteracy affect graduates long-term? Early financial missteps, such as an unnecessarily expensive loan or years without any savings habit, compound over time into materially lower lifetime wealth in much the same way as unpaid debt compounds against a borrower.

What do financially literate graduates do differently? They are more likely to maintain an emergency fund, evaluate borrowing decisions with the actual cost in mind, understand their payslip and tax obligations, and make long-term savings and investment decisions earlier rather than later.

How can universities add financial literacy to their curriculum? The most effective approach tends to combine a mandatory first-year module with integration into discipline-specific teaching, supported by experiential tools such as simulations or digital badging rather than lecture-only delivery.